SAN FRANCISCO, CA - Last week, the House Republicans released their much-anticipated tax reform proposal. The plan proposes to cut the corporate tax rate to 20 percent from 35 percent and reorganize individual tax rates from seven brackets into four. Taxes are a complicated subject, and with any sweeping change such as the proposed reforms, the devil is in the details. While the proposal promises to save an American family an average of $1,182 per year, some of the proposed changes could be devastating for current and future California homeowners.

SAN FRANCISCO, CA - Last week, the House Republicans released their much-anticipated tax reform proposal. The plan proposes to cut the corporate tax rate to 20 percent from 35 percent and reorganize individual tax rates from seven brackets into four. Taxes are a complicated subject, and with any sweeping change such as the proposed reforms, the devil is in the details. While the proposal promises to save an American family an average of $1,182 per year, some of the proposed changes could be devastating for current and future California homeowners.

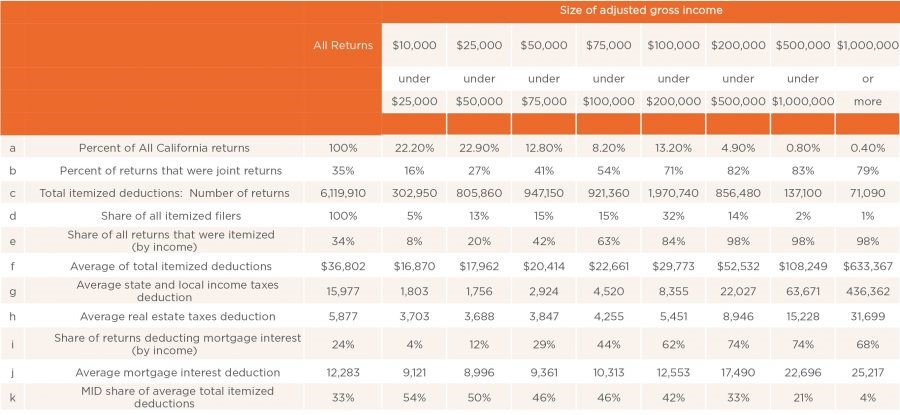

To understand the impact of these proposed changes on Californians, let’s examine the distribution of tax filers, as well as what type and the amount of itemized deductions they take. Figure 1 contains 2015 IRS individual income and tax data for California filers.

Since the tax proposal increases the standard deduction from $6,350 to $12,000 for individuals and from $12,700 to $24,000 for married couples, we’ll focus on the filers who itemize their deductions and will consequently be affected by the proposed changes. Thirty-four percent, or about 6.12 million California taxpayers, itemized their deductions in 2015, with average total itemized deductions equaling about $36,800. Thus, for those 34 percent of tax filers, losing some of the proposed deductions would make a notable difference in their adjusted gross incomes.

Figure 1: 2015 IRS individual income and tax data for California filers.

Source: IRS, Statistics of Income Division, Individual Master File System, August 2017.

Admittedly, things are a little more complicated than the numbers suggest. For filers with adjusted gross incomes of less than $75,000, who comprise 35 percent of all itemized returns, averages of total itemized deductions (row f) do not exceed the $24,000 proposed deduction for couples. Nevertheless, those filers are more likely to be single, (row b), in which case the proposed standard deduction of $12,000 would apply. Interestingly, only 35 percent of all California tax filers are joint returns. That share increases to 50 percent and higher among taxpayers with adjusted gross incomes above $75,000.

Thus, even for single filers with adjusted gross incomes below $75,000, their average total itemized deductions exceed $12,000. Hence, they stand to lose some of the deductions from proposed changes. The largest impact stems from losing the state and income deductions, since this group of filers generally does not pay real estate taxes of more than the $10,000 cap. In terms of the mortgage interest deduction, since the proposed cap would apply to newly originated mortgages going forward, current borrowers would not be affected. However, homebuyers with gross adjusted incomes of less than $75,000 could choose to purchase properties priced below $625,000 to maximize on their mortgage interest deduction, although they may not be able to qualify unless they have a substantial down payment.

However, the proposed tax changes could be more disadvantageous for those with incomes over $75,000, who comprise two-thirds of itemized filers and one-third of California returns. In the Bay Area, about 46 percent of households earn more than $100,000 and about 30 percent earn between $100,000 and $200,000. Also, home prices in the Bay Area are well above $625,000, which means that the mortgage interest deduction cap (assuming a $500,000 mortgage loan with 20 percent down) would be more impactful.

Figure 1, row f shows the average of total itemized deductions, which average between about $23,000 and $53,000 for gross adjusted incomes between $75,000 and $500,000. Simply eliminating state and income taxes may be most arduous for filers earning between $100,000 and $200,000 and $200,000 and $500,000. As row g suggests, 28 percent to 42 percent of their total deductions come from state and local income taxes. Among all returns, the value of state and local deductions comprises 43 percent of the total value of itemized deductions. If those are removed for the $200,000-to-$500,000 adjusted gross income group, the remaining deductions come close to standard deductions (assuming joint returns, which most of them are, according to row b). For the $100,000-to-$200,000 bracket, which is a large percentage of Bay Area households, losing the state and local income tax deductions removes the need to itemize deductions, since the remaining deductions fall below the standard $24,000 limit. All in all, removing the ability to deduct state and local income taxes markedly increases bills for most Bay Area residents.

Further, while the mortgage interest deduction averages $12,283, and 24 percent of all returns deduct the mortgage, the proposed changes are more impactful on the future homebuyers and the housing market in general since the proposed changes would apply to newly originated mortgages.

Over the last year, 70 percent of Bay Area homes sold were priced above $625,000, and 30 percent were priced higher than $1.2 million. Those two price benchmarks represent mortgages between $500,000 and $1,000,000, with an assumed 20 percent down payment. Thus, 70 percent of home sales are at a potential loss from changes to the mortgage interest deduction. Granted, about 26 percent of transactions below $1 million were all cash in the Bay Area , according to our recent analysis; however, that share was smaller in markets such as San Francisco, Silicon Valley, and the East Bay. All-cash buyers are more likely to purchase homes priced above $2 million, and only 13 percent of cash buyers were first-time buyers.

Nevertheless, the lower cap on the mortgage interest deduction would be particularly detrimental to first-time buyers in in the Bay Area. For example, a buyer of a $1.2 million home with a $1 million mortgage would pay almost $40,000 in amortized interest in the first year. However, at the $500,000 mortgage interest deduction cap, the buyer would be able to deduct only half of that interest, thus losing about $20,000 in deductions. Again, if this is a first-time buyer and likely to fall in the income range of between $100,000 and $200,000 in the Bay Area, the loss of a $20,000 mortgage interest deduction would make a notable difference, not only in the resulting tax bill but also on the decision to purchase a home. Also, note that while the proposed tax plan reduces the number of brackets, not everyone’s tax rate will decrease, and these deductions will play a big role in where a household falls along the income spectrum.

Furthermore, a $10,000 cap on real estate property taxes would also impact those buying a home priced above $1 million since California property taxes generally average about 1 percent. Again, in the Bay Area, 36 percent of home sales year to date were priced higher than $1 million. For example, a buyer of a $3 million home would lose $20,000 in property-tax deductions. Six percent of San Francisco sales and 7 percent of San Mateo County sales are priced above $3 million.

Figure 2: Home sales by price point in Bay Area counties

Source: Pacific Union transaction questionnaire. Results based on 4,266 responses collected between Jan. 1, 2016 and May 31, 2017. Updated Aug. 7, 2017.

Moreover, with proposed changes impacting future homebuyers, current homeowners are less incentivized to sell, which would further intensify the severe inventory shortage in the Bay Area — especially for more affordable homes.

In addition, the proposed change that limits the capital-gains exemption used by homeowners when they sell would be another major blow for supply conditions. Under the new proposal, homeowners must have owned and lived in the home for at least five of the last eight years to qualify for the exemption. Currently, the rule is two of the last five years. The exclusion would also be limited to one sale every five years rather than one sale every two years. In addition, households with incomes over $500,000 if married or $250,000 if single lose the exclusion. With the current capital-gains exemption limit at $500,000, it already poses a constraint on many current owners whose homes have appreciated significantly since they purchased them and who consequently choose not to sell. Further limiting the use of the capital-gains exemption will slow housing turnover even more. At the end of the day, while severely undersupplied inventory may help push prices higher, the proposed changes would lead to fewer home sales and an even more difficult environment for first-time buyers.

Taken together, the proposed tax reforms are a serious concern for Bay Area homebuyers and the future of the housing market. Again, the proposal is still under revision, and Republicans have started making changes.

Ultimately, we may or may not see some form of tax reform pass. Admittedly, the changes discussed here are somewhat simplified, and not all proposed changes have been evaluated. Also, this analysis does not include the potential impacts on corporate taxes, charitable deductions, or pass-through organizations. Overall, we would urge caution moving forward with the proposal as it currently stands.