By Tim Estin with Coldwell Banker Mason Morse

By Tim Estin with Coldwell Banker Mason Morse

The Estin Report: 3rd Quarter 2012 State of the Aspen Real Estate Market by Tim Estin with Coldwell Banker Mason Morse

This report documents sales activity for the 3rd Quarter and Q1-Q3 2012 (Year-to-Date) for the upper Roaring Fork Valley - Aspen, Snowmass Village, Woody Creek and Old Snowmass. Included property types are single family homes, condos, townhomes, duplexes and residential vacant land at sold prices over $250,000. Fractionals are not included. It compares the 3rd quarter to the same prior year quarter and to historical data since 2004, and Q1-Q3 2012 to the same prior year period. There are three sections: the Aspen/Snowmass total combined market, the Aspen market (includes small Woody Creek and Old Snowmass areas) and the Snowmass Village (the ski resort) market. The source data is from the Aspen/Glenwood MLS. Abbreviations: Aspen (ASP) - which includes Woody Creek (WC) and Old Snowmass (OSM); Snowmass Village (SMV).

Click here for the full third quarter report in PDF

Total Aspen Snowmass Market*

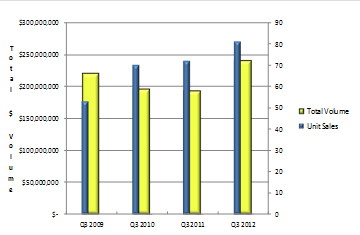

3rd Quarter 2012

In the 3rd Quarter 2012 (July 1st - September 30th), total dollar sales volume was up 25% and total unit sales were up +13% over the 3rd Quarter 2011 for the combined Aspen and Snowmass Village real estate marketplace. This has been the strongest performing 3rd Quarter in the past 4 years. Aspen single family home sales were especially strong, up 46% in dollar sales and up 22% in unit sales during the 3rd Quarter over the same time last year.

Prior Year 3rd Quarter Comparisons

©The Estin Report: Q3 2012 www.EstinAspen.com

Q3 2012:

- $240.4M (+25% from Q3 2011)

- 81 unit sales (+13% from Q3 2011)

Q3 2011:

- $192.6M dollar sales (-1% from Q3 2010)

- 72 unit sales (+3% from Q3 2010)

Q3 2010:

- $195.2M dollar sales (-11% from Q3 2009)

- 70 unit sales (+32% from Q3 2009)

Q3 2009:

- $220.1M dollar sales

- 53 unit sales

Q1- Q3 2012

In the first three quarters of 2012, (Jan. 1—Sept. 30th), the total Aspen and Snowmass combined dollar sales volume was off –12%, unit sales were even with last year , 0% change, and inventory of properties for sale decreased –6% compared to the same period last year.

The drop in dollar sales can be attributed to 30% fewer sales of over $10M homes this year versus last: in Q1 - Q3 2012, there were (9) sales over $10M at a value of $133M; in the same period 2011, there were (13) sales over $10MM at a value of $240M. This -$107M difference accounts for almost the entire dollar sales difference between Q1-Q3 2012 compared to Q1-Q3 2011 for the total Aspen Snowmass Village market combined.

Why fewer ‘big ticket’ sales? A number of new large spec homes were sold at significant discounts in the past 1-3 years by strained developers and builders, and this inventory of highly pressured-to-sell ultra luxury homes has mostly been depleted.

Comments

In each of the past three years, after relatively favorable starts at the beginning of year, the national economy sputtered in the 2nd quarters due mostly to uncertainty caused by shifting employment numbers, sovereign debt, Euro concerns, and domestic political impasse.

In spite of this, the 3rd Quarter 2012 proved to be remarkably strong in general but especially in the sales of Aspen single family homes. While Aspen total dollar sales account for 83% of the entire Aspen and Snowmass Village dollars combined, Aspen single family homes sales account for a whopping 56% of the total combined market dollars.

Aspen Single Family Homes

Sales of Aspen homes were up 46% in dollar volume and 22% in unit sales for the 3rd Quarter over the same period last year.

Single family home pricing pressure appears to have eased through the 3rd Quarter 2012: median prices, generally a more accurate indicator of pricing trends as average prices can be skewed disproportionately by very high or low sold prices, are up marginally, 3% , to $3.8M in Q3 2012 versus $3.7M last year same time; single family home price per sq ft increased +13% to $1,013 sf in Q3 2012 from $899 sf same time last year arresting the downward trend of the past 4 years.

Both metrics — median prices and price per sq ft — can be seen as positive signs of home price stabilization.

Aspen Condos

Aspen condo unit sales were up 30% in Q3 2012 from the same period last year, (30) sales now versus (23) then, but dollar sales volume, was -26% lower at $33M in Q3 2012 versus $44M same time last year.

Sales up; dollars down...Reason? Of the (30) condo sales, 70% of them, (21) units, were one and two bedroom units selling at under $1M and much smaller in physical size than those sold last year, -39% smaller, at an average 1,078 sq ft this year versus 1,755 sq ft last year.

Consequently, the median Aspen condo price in Q3 2012 decreased a dramatic -34%, to $757,000 from $1.1M vs same time last year, and the average price per sq ft fell -12% to $904 sf in Q3 2012 from $1,033 sf last year. Unless a condo is a pristine or new remodel, buyers are moved by value primarily. Like-new condition, recent remodels and the best deals sell, all others languish on the market.

Snowmass Village

Snowmass Village real estate has fallen hard in the past four years. This is largely due to the very real excitement surrounding the resort in 2005-2007 as the Related Companies took over the new Base Village development. The Snowmass resort was to be reborn. As the excitement escalated, so too did prices. Then the crisis hit and it all unraveled.

Snowmass total dollar sales in Q1-Q3 2012 (YTD) are $83M versus $129M same time last year, or –36%, and this is -63% off the $304M dollar sales peak in the same period in 2007; unit sales now at 52 are off from 62 units sold same time last year, –16%, and off –66% from the average 153 units sold in the Q1-Q3 periods of the peak years 2005-2007; the average price per sq foot of a single family home at $690 sf now is off –20% from $858 same time last year which is -52% from its 2007 peak of $1,430. For condos, the avg. price per sq ft is down –1% from $630 sf now from $637 same time last year, and off –42%, from the peak of $1,080 sf in 2007.

All of which is to say that unbelievable deals are to be had in Snowmass ...and there are reasons for optimism.

- Related Co's buy back in Sept. 2012 of the Snowmass Base Village from German banks paves the way for the future development of the resort. As one reporter recently wrote, "the recent and complicated buy-back of the commercial properties by Related Companies (through its Snowmass Acquisition Company LLC) shows that major investors are once again willing to sink big bucks into Snowmass. Will that lead the way for smaller investors to step forward and take a risk too?" At the very least, it creates a positive foundation for new development and more positive news moving forward.

- The slope-side Silvertree Hotel has new owners and is now run under the Westin brand after $55M improvements were put into the Snowmass Mall and conference hotel facilities in the past year. It is a month early in its completion and all systems are go for winter 2012/2013. Add to this the beautiful, contemporary Viceroy Hotel which opened Nov. 2009 and the SMV hotel ski-in out experience offers serious competition to Aspen's limited ski in/out hotel offerings.

- Snowmass Village prices in general are off an average 40% - 50% from the 2007/2008 market peak. With an ample supply of units - 78 single-family homes and 157 Condos/townhomes for sale as of this writing (Oct. 14) the best buyer values in the Aspen area are here.

- SMV condos represent great value at today's prices as most are located at or near slope-side with an excellent ski in/out experience and rental income opportunities.

- There are numerous SMV single family home opportunities for prospective Aspen School District buyers and for those seeking the highest quality ski in/out homes at market corrected prices on top of the 20-30% historical discount Snowmass properties have offered compared to Aspen.

Now, during the off-season - before the high tourist winter ramps up and at the cusp of a clearer path forward for the Base Village - is the time to buy in Snowmass Village.

Vacant Land Sales Surging

There has been a dramatic increase in vacant land sales this year and it continues. Through the 3rd Quarter, Sept 30, 2012, there have been 23 land sales this year versus 12 last year same period, +92%. The dollar value of these sales has jumped to $65M this year from $27M, +144%. This does not include the sale of older teardown properties which appear in the MLS as residential property with improvements not vacant land. Buying land and building new offers a reasonable hedge against continued market uncertainty and against the slow pace of an improving marketplace. As there is relatively little new construction occurring at present due to uncertain macro conditions and still difficult but improving loan qualification conditions, by the time one completes construction of a new Aspen home in 18—24 months, demand for this scarce product should be high, supply low and premium pricing a realistic outlook. As mentioned in earlier reports, typically, when land sales start to pick up, it is an important marker of a market transition, a tipping point.

*Includes upper Roaring Fork Valley: Aspen, (with Old Snowmass, and Woody Creek) and Snowmass Village (SMV) combined, all residential properties and vacant land—all over $250,000. Fractional sales are not included.